Insights

Physician Groups Must Act on Value-Based Payment

By Jeff Swearingen and Saskia Siderow –

For physician groups, the days of “practice as usual” are over. Radical changes to how doctors are paid for their services – long a matter for academic debate or incremental policy fixes – are now a reality, with profound implications for the way doctors conduct the business of their medical practice. To survive and thrive in the new value-based payment landscape, physician group leaders need to invest substantial time and capital in electronic health records, data analytics, care coordination, physician engagement and other quality improvement initiatives. These projects require design, implementation and ongoing management to meet performance metrics – none of which was taught in medical school and all of which will drastically reduce how much time practice leaders can spend with their patients.

Worryingly, many physician groups feel under-prepared or under-resourced to make these changes,1 or simply don’t appreciate the urgency or relevance of healthcare transformation for their own practices. Granted, under new Medicare legislation passed in 2015, smaller practices are exempt from value-based payment regulations for now, and current financial penalties for non-participation or under-performance have yet to ramp up. Physicians have also eyed the political debate over the future of the Affordable Care Act as a reason to “wait and see.” This is particularly the case when it comes to expensive and burdensome projects such as electronic health records (EHRs), which doctors widely perceive as adding little clinical value for patients and greatly contributing to physician burnout.2

But the pace of change is accelerating and time is running out for physician groups to take the necessary steps to safeguard their futures. Below, we dispel three of the most common misconceptions about the transformation in healthcare to underscore that now is the best time to act.

“Why tackle payment reform and quality reporting now? Healthcare is a hot button political issue and everything could change after the 2020 election…”

Value-based payment is here to stay, no matter who occupies the White House after 2020. The United States spends drastically more on healthcare per capita and as a percentage of GDP than any other developed country, in exchange for below average outcomes. An aging population is living longer with chronic conditions amid rising healthcare costs. By 2030, the number of Americans over the age of 65 will be greater than the number of people of working age for the first time in history. Improving value in healthcare – solving for how to achieve the best healthcare outcomes at the lowest cost – is an urgent bipartisan effort.

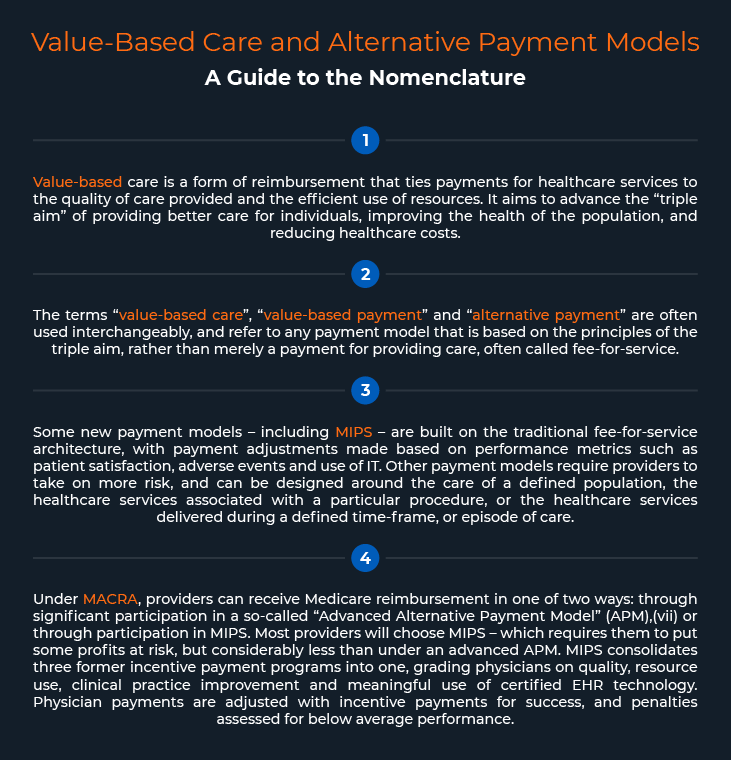

Healthcare policy will, without a doubt, be one of the key issues that drives voters in 2020. The debate over the strengths and flaws of the Patient Protection and Affordable Care Act, passed by a hair in 2010, is heated and will remain so into the election cycle. But that debate is focused on healthcare access and affordability, particularly with respect to insurance coverage and drug pricing, and not on the manner in which healthcare is reimbursed. Unlike the ACA, the 2015 Medicare Access and Chip Reauthorization Act (MACRA), which legislates payment reform for Medicare, was passed with overwhelming bipartisan support. The law replaced the extremely unpopular “sustainable growth rate” formula for physician reimbursement and was passed with a 392-37 vote in the House and a 92-8 vote in the Senate. As contentious as US politics has become in recent years, physicians must plan on MACRA’s new framework for physician payment.

The keystone of MACRA’s new framework is the Merit-Based Incentive Payment System (MIPS). MIPS has had a phase-in period to help physicians prepare, and the first payment changes will take effect this year. Physician practices’ 2019 Medicare revenues will be affected by an up to 4% penalty based on 2017 reporting and penalties are set to increase to up to 9% for the 2020 reporting year. Given that many provider organizations have single-digit profit margins on their Medicare Part B patients,3 potential MIPS penalties pose a significant threat to financial sustainability for non-performing practices. In contrast, early adopters will have a substantial competitive advantage over their peers: not only does CMS plan to raise performance thresholds annually and publish physicians’ performance scores, but a significant portion of MIPS incentive payments for performing physicians are paid from the penalties assessed on non-performing physicians. Physician groups that prepare for MIPS and earn incentive payments will be those that are in a position to consolidate, while groups that delay will see their value significantly impaired.

Exemptions from MIPS still leave physicians in a pinch. Although many small physician groups are exempt from MIPS during the phase-in period,4 CMS intends to steadily include all physicians in the program. Under MACRA, physicians will not receive any payment adjustment for inflation from 2020-2025, meaning that reimbursements will not keep pace with the average rate of physician cost increases, further eroding razor-thin margins.

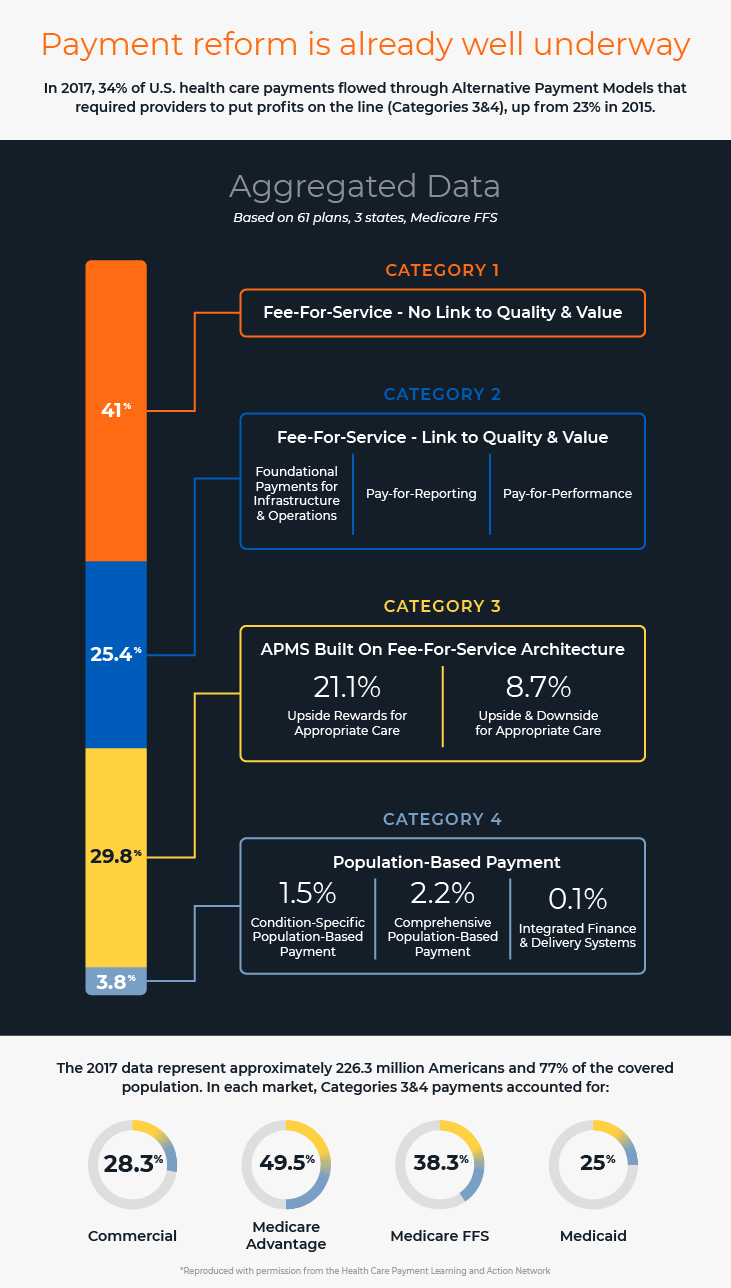

Importantly, Medicare payment policy is also a bellwether for the other payors. Many commercial payors have made public commitments to increasing their participation in value-based payment models, and several large commercial insurers such as UnitedHealth Group, Aetna and Cigna already have over 50% of their spending tied to value-based care.5 In 2017, 34% of all US health care payments were tied to alternative payment models, up from 23% in 2015.6 The shift to payment for value is unavoidable.

“Healthcare transformation projects are more important for large hospitals and health systems than physician groups”

One of the consequences of the shift to value-based payment is that payors and health systems are increasingly focused on moving patients to lower acuity sites of care whenever possible. In multiple studies, this has demonstrated lower costs and improved quality metrics such as patient satisfaction and infection rates. The trend has prompted health systems to buy up specialty physician practices so they can control the continuum of care for their patients, or to partner with physician groups that can demonstrate with verifiable data and reporting that their practices are producing the desired outcomes. As more and more reimbursement is tied to episodes of care or fully capitated under alternative payment models, physician groups will fall to the bottom of the referral list if they are unable to deliver on health system quality and cost measurement and performance. The ability to demonstrate value will be key to physician group survival.

“We can wait, strategic partners will be available if we need them.”

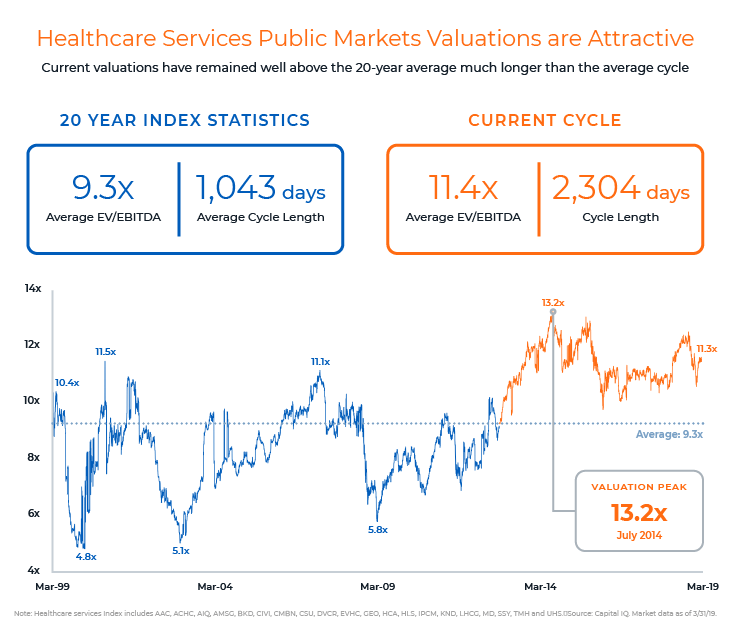

Healthcare transformation is driving substantial vertical and horizontal consolidation in the healthcare industry, with few signs of the trend abating. Recent transaction volume suggests there is still considerable interest in physician groups among potential strategic partners – including but not limited to health systems, payors, peer physician groups and private equity funds. Last year saw 250 announced transactions, a 51% increase over 2017, and since 2012, consolidation has accelerated at a rate well in excess of previous periods, indicating a sense of urgency not previously seen. The level of interest has been good for valuations, as more investment firms have entered and committed funds to the healthcare sector. Current valuations have remained well above the 20-year average for much longer than the average cycle.

In the spirit of “an ounce of prevention is better than a pound of cure,” the best time for physician groups to consider their strategic alternatives is before they have to, when options will be far more limited. Market cycles are notoriously hard to predict, but with current conditions so attractive, physician groups would do well to examine their options now. There are no guarantees that strategic partners and attractive valuations will be available for those who wait.

Whether they want to remain independent, attract a buyer or partner, or buy up practices themselves, physician practices have to adapt to survive in the new value-based payment world. Successful practices will have access to capital, an established IT infrastructure and be data driven. Accomplishing these goals may mean pursuing a strategic business plan focused on growth, or pursuing a transaction – perhaps with a healthcare system, another medical group or a private equity investor. It’s important to seek good advice because the right solutions will differ depending on the practice specialty, patient volume and preferences, and different groups will weigh the risks and benefits of each option in their own way. Since choosing to wait for a strategic partner is still a choice, it’s worth ruling out the alternatives to make a fully informed decision.

________________________

Jeff Swearingen is co-founder and Managing Director of Edgemont Partners, an independent healthcare investment banking firm in New York. Jeff has focused on healthcare for his entire career, since starting as an accountant at KPMG’s Healthcare and Life Sciences Group in 1994. He co-founded Edgemont in 2001 and leads Edgemont’s clinician advisory practice.

![]()

Saskia Siderow, MPH, is founder and Managing Director of Ormond House, a healthcare services research and strategic communications consultancy.

About Edgemont Partners

Edgemont Partners is a premier investment bank that provides merger and acquisition advisory and growth capital raising services exclusively to healthcare companies. We focus solely on providing expert strategic advice and transaction execution, bringing a steadfast commitment to our clients, driven always by what’s in their best interest. This dedication enables us to deliver independent conflict-free advice, to serve as trusted advisors to healthcare entrepreneurs, management teams and investors, and to execute with exceptional results.

________________________

1 Friedberg, Mark et al. “Effects of Health Care Payment Models on Physician Practice in the United States: Follow-Up Study”, American Medical Association, October 24, 2018.

2 Stanford Medicine and The Harris Poll, “How Doctors Feel About Electronic Health Records”, National Physician Poll condicted March 2018.

3 Lee, Tom; “Gauging the Financial Impact of MIPS”, Healthcare Financial Management Association, May 16, 2017.

4 Clinicians are exempt from MIPS if they meet one of three criteria: (1) they are in their first calendar year of Medicare Part B participation; (2) they bill $90,000 or less in Medicare Part B charges, provide fewer than 200 covered services or provide care for fewer than 200 beneficiaries; (3) they participate in an advanced APM.

5 Japsen, Bruce; “Cigna Eclipses 50% in Value-Based Care Pay to Providers”, Forbes.com, February 7, 2019

6 Health Care Payment Learning and Action Network, “Measuring Progress: Adoption of Alternative Payment Models in Commercial, Medicaid, Medicare Advantage and Fee-for-Service Medicare Programs”, October 2018.

7 Qualifying APMs include Medicare Shared Savings Plans with both upside and downside risk (Tracks 2 & 3), Next Generation Accountable Care Organizations (Tracks 1 & 2) and a Patient-Centered Medical Home Model (Comprehensive Primary Care Plus)